Award-winning PDF software

form 12277 (rev. october 2011) - internal revenue service

You do not have to answer any particular questions if your lien is not valid or your property is not being listed on the lien. Your filing status will be changed to exempt filing status because a tax lien has been released. This may change your tax payment status. Your filing status will be changed to the following if you have met the requirements for a Notice of Federal Tax Lien. Your filing status will be changed to an exempt status as a result of a Notice of federal tax lien. Your filing status will be changed to exempt status if: You completed the notice of federal tax lien and filed your federal taxes with us. If your filing status is exempt, you can either mail a copy of the notice of federal tax lien or, if required by IRS, download the PDF version of the notice of federal tax lien and.

Understanding a federal tax lien | internal revenue service

And, if applicable, Form 8829, IRS Notice of Tax lien (Internal Revenue Code Section .09). If you are an attorney or officer of a federal, state, local or foreign government, the notice you are required to file with the Internal Revenue Service is available on Q. When do I file Form 668 for the delinquent FEDERAL ASSISTANCE (FAST) TAX on my business income? A. If you are filing as a sole proprietor and fail to timely, timely pay any FEDERAL ASSISTANCE tax liability on business income your account, check one box on Form 668 and, if applicable, refer to Form 8829, IRS Notice of Tax lien (Internal Revenue Code Section .09). FEDERAL ASSISTANCE tax is NOT due until the payment or other payment is made. The date you need to file is 6 months from the last date you are aware of when your deficiency (if any) is paid. In calculating your.

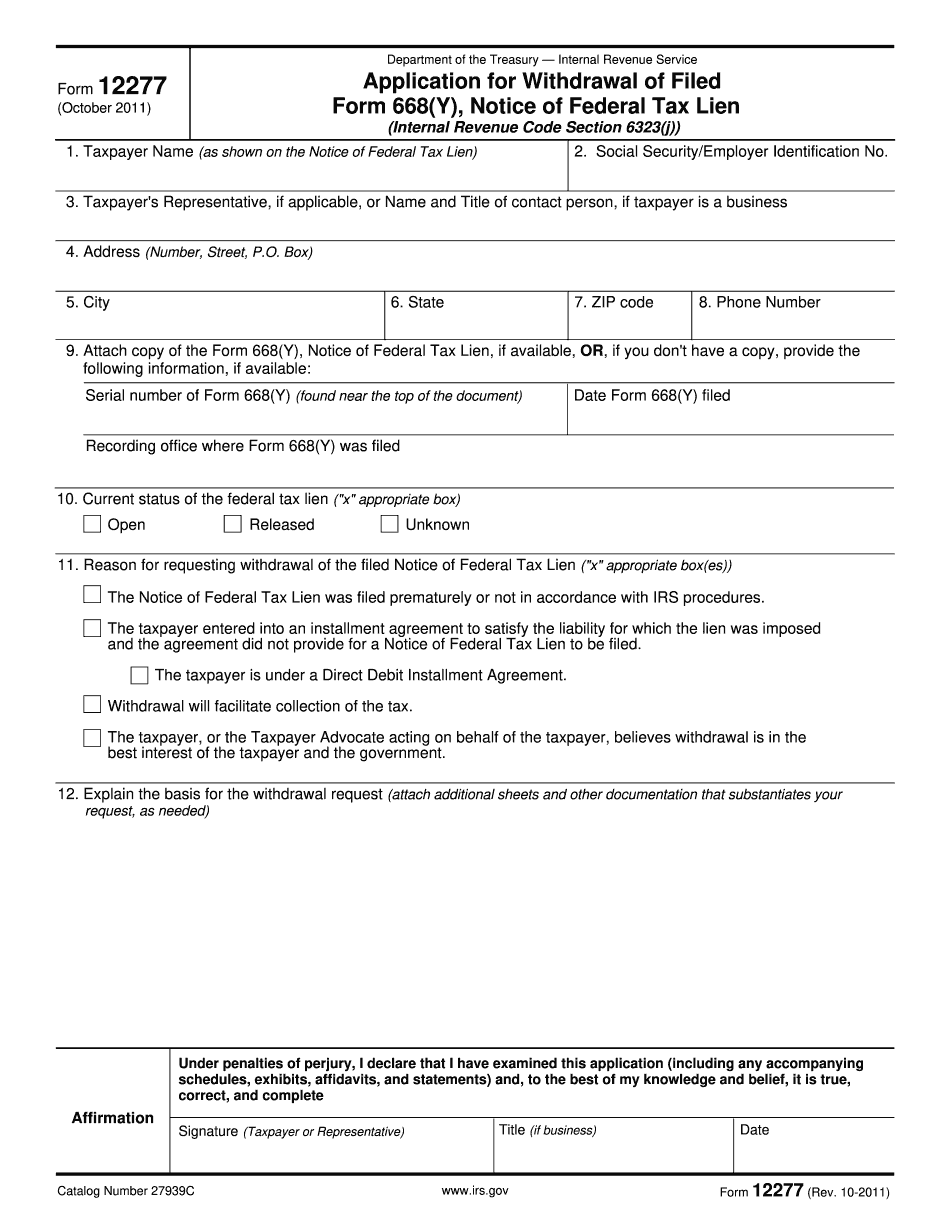

form 12277: application for withdrawal of filed form 668(y)

PDF of a debt from a past financial institution, which, according to IRS definitions, is also referred to as a “Tax Lien” on account of the taxpayer's tax debt. There are three components to the NFL for IRS collection purposes. The first, the collection address, is generally the same as the taxpayer's current address. A second, the notice text is sent by IRS to the taxpayer, via an Email or paperless submission in the future. And, the third component, the amount of the outstanding debt, may be deducted from income in accordance with the provisions of IRC 6103 and IRC § 6109(a). The NFL is therefore quite simply a “debt” that can be removed by the taxpayer as part of ordinary tax procedure.

form 12277: application to withdraw federal tax lien from

Gov Form 2848 and fill it out. The form gives you instructions on how to contact the IRS at the number given and tell them you want them to remove a lien or refund it to you from your credit report. Step One —. . . The IRS has no way of knowing who your creditor was in the first place! The IRS can't “track” when and where your debt was filed (which is why they require written notification), can't determine who filed your tax returns. Step Two: In case you want the IRS to stop (or lessen) your penalties and interest, and the tax lien is in fact the ONLY tax lien on your record, take a copy of your credit report to a local law firm with professional representation in dispute resolution. You may be able to settle this matter out of court and end up.

Lien notice withdrawal - video portal

It asks if you want the IRS to look at other people's assets. That's an awful lot to ask. In most cases, the IRS does the right thing: it does the same thing in all situations. But if the government has a lien against your assets, it ought to look at those assets before seizing them or putting liens on them. The lien is a court judgment against you. It is a way of saying, “Go get this.” You can take your case for recovery of these funds to court. The statute of limitations on filing such a proceeding ends one year after the filing. And the IRS will generally take you to court if you haven't filed a lawsuit within that one-year period. It probably won't sue you if you file a suit within one year of the filing date, though: there just aren't any federal lien laws that.